What Does It Mean to Provide Liquidity for Crypto in 2026?

It starts with a simple question: can you actually trade this thing?

Liquidity, at its core, is how easily you can buy or sell an asset without moving its price. In traditional markets, that's already tricky. In crypto, it's a whole different level of challenge.

The market never closes. Sentiment can flip in minutes. The same token trades across dozens of exchanges and DeFi protocols simultaneously. And if a project hasn't done the work to build a real market around its token, you'll feel it immediately - wide gaps between buy and sell prices, a chart that jumps on small orders, and the uncomfortable sense that you might not be able to exit when you need to.

Three things tell you whether a market is liquid or not:

The bid-ask spread - the gap between what buyers are willing to pay and what sellers are willing to accept. A tight spread means a healthy, competitive market. A wide spread is essentially a hidden tax on every trade you make. Order book depth - how much volume sits close to the current price. Deep books can absorb large trades without the price flinching. Thin books can't. Slippage - the difference between the price you expected and the price you actually got. This is the most honest measure of liquidity in practice. You can have a gorgeous-looking order book and still get crushed by slippage on anything over a few thousand dollars.

According to Bitgo's crypto liquidity research, liquidity is best measured by real execution costs effective spread, implementation shortfall, and slippage - not by quoted spreads alone.

So who actually provides this liquidity?

Here's where it gets interesting. "Liquidity provider" sounds like one thing, but in 2026 it covers a pretty wide range of participants.

At the professional end, you have market-making firms. These are specialist desks that deploy capital algorithmically - placing buy and sell orders continuously, adjusting quotes in real time, managing inventory risk around the clock. They profit from the spread, but they also carry real risk: if the market moves sharply against their inventory, they eat the loss.

At the retail end, anyone with a wallet can be a DeFi liquidity provider. You deposit tokens into a smart contract pool, and the protocol pays you a share of the fees every time someone swaps through that pool. It sounds passive and simple, and sometimes it is - but it comes with its own risks, which we'll get to.

Both models are trying to solve the same problem: make it possible for people to trade without waiting forever or paying through the nose. They just use very different tools to do it.

Want to see how this works in practice? Here's how BeLiquid structures liquidity programs for token projects.

How it works on centralized exchanges

On a CEX - Binance, OKX, Coinbase, Kraken - liquidity lives in the order book. Every resting limit order on either side of the market adds to it. Professional market-making desks post bids and asks across multiple price levels constantly, so when you come in to buy or sell, there's something waiting for you.

The difference between a well-supported token and a neglected one is stark. With proper market-making behind it, a token's book looks clean: consistent depth, predictable spreads, price that moves gradually rather than lurching on every moderate order. Without it, the book looks like a ghost town. Someone tries to buy $10,000 worth and the price moves two percent. That's a nightmare for investor confidence.

CEXs still dominate institutional trading. Fast matching engines, fiat on-ramps, familiar interfaces - for big players, these things matter a lot. But the quality of execution on any given token is only as good as the market-making behind it. The exchange itself isn't going to do that work for you.

How it works on DEXs - and why AMMs changed everything

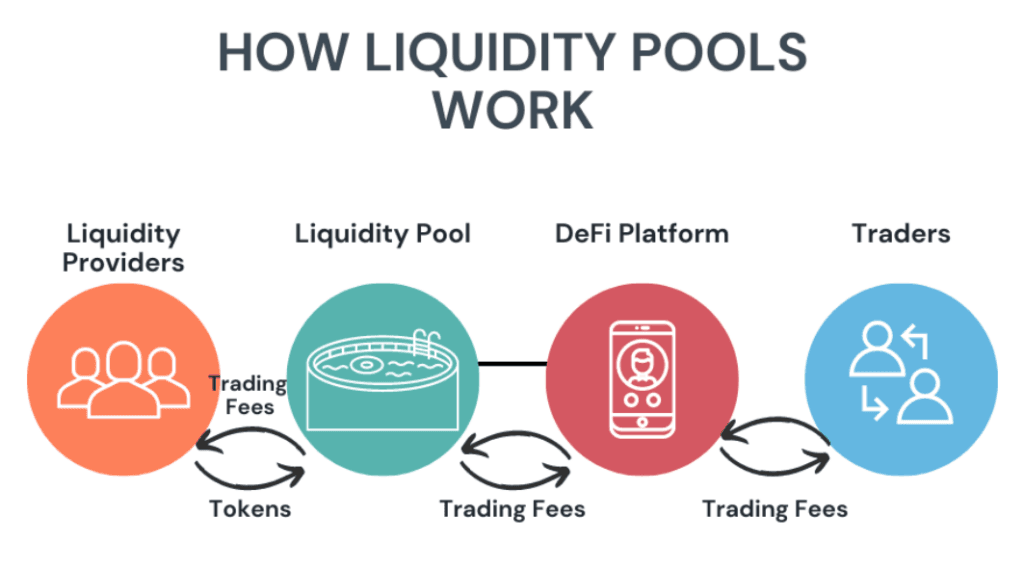

Decentralized exchanges took a completely different approach. Instead of matching buyers and sellers through an order book, they use liquidity pools and automated market makers (AMMs).

The basic idea: two tokens sit in a smart contract. When someone wants to swap one for the other, the contract executes it algorithmically, adjusting the price based on the changing ratio of the two tokens in the pool. The more of one token you take out, the more expensive it gets. Arbitrageurs then come in to close the gap between the pool price and the broader market.

The most common model uses a formula called x × y = k, where x and y are the quantities of the two tokens and k stays constant. It's elegant in its simplicity, and it works but it has one major flaw for liquidity providers: most of the capital is spread across price ranges where almost no trading ever happens.

Uniswap V3 fixed this in 2021 with concentrated liquidity. Instead of spreading your capital across all possible prices, you choose a specific range - say, $2,500 to $3,500 - and deploy your capital only there. If most trading happens in that band (which it usually does), you earn a much larger share of fees per dollar deployed. Uniswap V4, launched in 2025, went further with programmable "hooks" - and according to DeFiLlama data, it crossed $1 billion in TVL in just 177 days.

DEX volume has more than doubled between 2024 and 2026 and now accounts for roughly 20% of global spot trading. That's not a niche anymore.

The risks nobody talks about enough

Providing liquidity sounds like a good deal. You deploy capital, the protocol pays you fees, everyone wins. And sometimes that's exactly how it goes. But there are real risks that get glossed over.

Impermanent loss is the big one. When the prices of the tokens you've deposited diverge after you put them in the pool, the AMM rebalances automatically - which means you end up holding less of the token that went up and more of the one that went down. Your position is worth less than if you'd simply held both tokens in your wallet.

It's called "impermanent" because it reverses if prices return to where they were when you deposited. But if you withdraw while they're still diverged, the loss is very real and very permanent. According to research published in the Journal of the British Blockchain Association, exchange fees and position duration are among the key variables that determine whether an LP actually comes out ahead. For a concrete example: imagine you deposit into an ETH/USDC pool when ETH is at $2,000. ETH then doubles to $4,000. The pool has been selling your ETH as it rose, because the formula requires it to rebalance. You're left with less ETH and more USDC than you started with, and the math often doesn't work in your favor.

MEV and front-running are another issue. Bots analyze pending transactions and reorder or insert trades to extract value at the LP's expense - what researchers call loss versus rebalancing (LVR). This is particularly damaging on concentrated positions. On the CEX side, inventory risk is the equivalent concern. Market makers hold token inventory, and when prices move sharply against them, losses can accumulate faster than spread income covers. There's also smart contract risk - pools can be exploited, and when they are, there's no safety net. And with MiCA now in effect across the EU and new US frameworks taking shape, regulatory risk is becoming increasingly real for anyone operating professionally in this space.

What's actually changed in 2026

AI is now deeply embedded in market-making. The algorithms analyzing order flow, predicting short-term price movements, and adjusting quotes in real time have gotten significantly more sophisticated. This generally produces tighter spreads under normal conditions - but it also means liquidity can evaporate faster during stress, as AI-driven systems pull back simultaneously.

Real-world asset tokenization has gone from interesting experiment to real market. Government bonds, private credit, real estate - these are now being issued as blockchain tokens and plugged into DeFi protocols. According to rwa.xyz, active on-chain private credit alone exceeded $18.9 billion in late 2025, and Boston Consulting Group projects the tokenized asset market could reach $18.9 trillion by 2033. But tokenizing an asset doesn't automatically make it liquid - building a proper two-sided market for an RWA requires exactly the same infrastructure as any other token.

The line between CEX and DEX is blurring. What used to be a binary choice is becoming a spectrum. Liquidity strategies in 2026 increasingly need to work across both worlds simultaneously - and according to industry analysis from Nadcab, this CeDeFi convergence is one of the defining exchange trends of the year.

Institutions are fully here. The global crypto market cap is north of $3.5 trillion. Daily trading volumes run in the hundreds of billions. That's brought in a tier of institutional participants who demand professional-grade execution, compliance guarantees, and genuine depth - raising the bar for what "good liquidity" looks like.

What to actually look for in a liquidity partner

1. Verify depth, not optics. Request historical order book data, not just screenshots taken on a good day. You want to see what depth looks like at 3am on a Sunday, not just during prime trading hours.

2. Check cross-venue coverage. A beautifully maintained book on one exchange doesn't help if there's a price dislocation happening on three others simultaneously.

3. Understand exactly how they're compensated. Flat retainers, spread sharing, and loan-based models all have different incentive structures - and some of those incentives don't align with your project's interests. Loan-based models in particular carry a specific conflict worth understanding before you sign anything.

4. Ask what happens when things go wrong. Flash crashes, exchange outages, sudden high-volume selling - these are the moments that reveal whether a liquidity partner actually has your back or disappears when it gets hard.

5. Demand on-chain verifiability for DeFi positions. Pool addresses, LP token holdings, historical fee income data - not a proprietary dashboard with numbers you can't independently check.

6. Align with your tokenomics calendar. Token unlocks, TGE events, and listings all create predictable liquidity stress. A good partner structures their program around these milestones in advance, not after the fact.

Frequently asked questions

What's the difference between a market maker and a liquidity provider? A market maker actively manages buy and sell orders using algorithms, continuously adjusting quotes and carrying inventory risk. A passive DeFi liquidity provider deposits tokens into a pool and earns fees. At the institutional level in 2026, these roles increasingly overlap - the same desk often manages both CEX order books and concentrated AMM positions simultaneously.

Can you lose money providing liquidity? Yes. Impermanent loss can exceed the fees you earn, especially in volatile markets. For stable pairs like USDC/USDT, the risk is minimal. For volatile pairs, you need to model it carefully - or use a provider who manages the position actively on your behalf.

Why does a token project need a liquidity provider? Without one, your token's order book is thin, spreads are wide, and the chart looks bad. That makes it harder to get listed on top exchanges, harder to attract investors, and harder to retain them. A credible market is one of the most important things a project can build - and it doesn't happen by itself.

What is impermanent loss, in plain English? When you deposit two tokens into a DeFi pool and their prices move apart, the pool automatically rebalances - selling the one that went up and buying the one that went down. When you withdraw, you have less of the winner and more of the loser compared to just holding. If the divergence is big enough, you're worse off than if you'd never provided liquidity at all.

How does concentrated liquidity work? Instead of spreading your capital across every possible price, you choose a specific range where you expect most trading to happen. Your capital earns fees only when the price is inside that range - but it earns a much higher share of fees than a full-range position would. It's more efficient, but it requires active management.

Is providing liquidity profitable? It depends on the pair, the volatility, the fee tier, and how actively the position is managed. For stable pairs, it generally is. For volatile pairs, fees often don't cover impermanent loss unless you're running a sophisticated hedging strategy on top.

How BeLiquid thinks about this

We focus on market health, not market optics. There's a big difference between a token that looks liquid and a token that actually is. A manufactured chart - built on artificial volume, thin real depth, and spread mechanics that disappear when the contract ends - might hold up for a while. But it doesn't build anything. The moment conditions change, it unravels.

What we build: real two-sided books, spread discipline, and depth placed where genuine order flow actually appears - on CEX and DeFi both, because in 2026 you can't afford to ignore either one.

If you're working on a token launch or trying to improve an existing market, BeLiquid can help - from program design to 24/7 operation and fully transparent reporting